Adding just $100 per month in extra payments to a typical 30-year mortgage can cut 6+ years off the loan term and save more than $73,000 in interest. The mechanism is simple — extra payments go directly to principal, reducing both the loan balance and the interest charged on every future payment. This guide shows exactly how it works with real numbers and a free calculator to model your own situation.

How Extra Payments Actually Reduce Interest

Every loan payment is split between interest (the cost of borrowing) and principal (the amount you actually owe). Early in a loan, most of your payment goes to interest. Late in the loan, most goes to principal.

When you make an extra payment, the entire amount goes to principal. This reduces the balance the lender uses to calculate interest for the next month, which means more of your next regular payment goes to principal too. The effect compounds — one extra payment makes future payments slightly more effective.

The earlier in the loan you start extra payments, the more powerful this effect becomes. A $1,000 extra payment in year 1 saves more interest than the same payment in year 25.

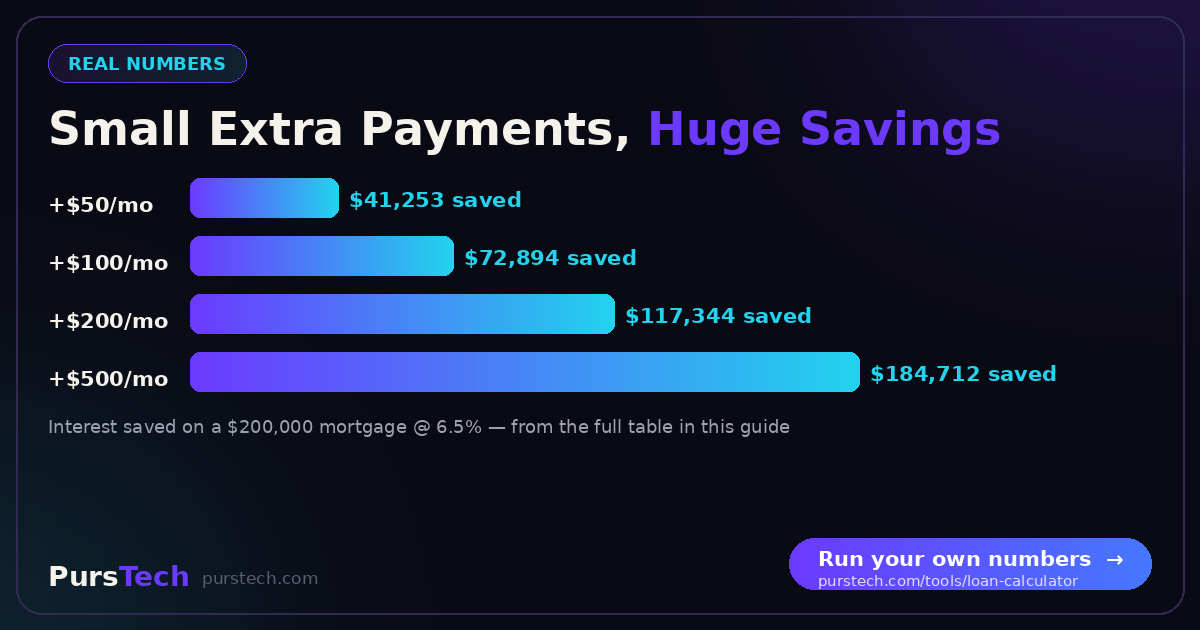

Real Numbers: How Much You Actually Save

The table below shows what happens to a $200,000 mortgage at 6.5% interest with different extra payment amounts:

| Extra Monthly Payment | Time Saved | Total Interest Saved | Total Cost |

|---|---|---|---|

| $0 (baseline) | — | — | $455,089 |

| $50 | 3 years, 7 months | $41,253 | $413,836 |

| $100 | 6 years, 2 months | $72,894 | $382,195 |

| $200 | 10 years, 1 month | $117,344 | $337,745 |

| $500 | 16 years, 8 months | $184,712 | $270,377 |

| $1000 | 21 years, 10 months | $222,876 | $232,213 |

The key insight: even small extra payments produce huge savings. An extra $100/month saves you almost 16% of your original loan balance in interest alone — money you can put toward retirement, investments, or anything else.

How to Calculate Your Own Savings

To see exactly how extra payments would work on your specific loan:

Step 1: Open the PursTech Loan Calculator.

Step 2: Enter your loan amount, interest rate, and term in years.

Step 3: Add the extra monthly payment amount you're considering.

Step 4: Compare the standard amortization schedule to the accelerated one.

The calculator displays total interest paid, total cost of the loan, and the new payoff date side-by-side, so you can immediately see the financial impact.

When Extra Payments Make the Most Sense

High-interest debt: Credit cards (15-25%), personal loans (8-15%), and older mortgages (above 6%) benefit most from extra payments because the interest savings are largest.

Long-term loans: 30-year mortgages and 7-year auto loans have huge amounts of interest baked into them. Extra payments cut this dramatically.

Stable income situation: If you have an emergency fund covering 3-6 months of expenses, extra payments are a smart use of additional income.

No higher-priority debt: Always pay down higher-interest debt first. A 22% credit card debt costs you more than extra payments on a 6% mortgage save you.

When NOT to Make Extra Payments

You lack an emergency fund: Money sent to a mortgage cannot easily be retrieved. Build 3-6 months of expenses in liquid savings first.

You have higher-interest debt: Credit cards, personal loans, and student loans often have higher rates than your mortgage. Pay those first.

Your loan has a prepayment penalty: Some loans charge a fee for paying off early. Read your loan documents — penalties can wipe out the interest savings.

You can earn more investing: If your investments reliably return more than your loan interest rate (after taxes), the math favors investing. This is rare in high-rate environments but worth checking.

You are near the end of the loan: Once most of your payment is already going to principal, extra payments save less interest. In the last 5 years of a mortgage, the marginal benefit drops significantly.

Three Effective Extra-Payment Strategies

1. Round up every payment. If your monthly payment is $1,847, pay $1,900. The $53 extra adds up to over $600 per year going straight to principal, with almost no impact on your monthly budget.

2. Make one extra payment per year. Use a tax refund or annual bonus to make one full extra mortgage payment each year. This single change shortens a 30-year mortgage by approximately 4-5 years.

3. Apply windfalls to principal. Inheritances, gifts, and large bonuses can make enormous progress when applied as lump sums. A single $10,000 lump sum in year 5 of a 30-year mortgage saves about $20,000 in interest over the life of the loan.

Make Sure Extra Payments Go to Principal

Most lenders default to applying extra payments to next month's regular payment rather than to the principal balance. This is why specifying "principal-only" is crucial.

Methods to ensure correct application:

• Use your lender's online portal — most have a "principal payment" option

• Write "Apply to Principal" on the check memo line

• Send extra payments as separate checks, not combined with your regular payment

• Check your statement the following month to confirm the balance reduced correctly

The Bottom Line

Extra payments are one of the most reliable ways to build wealth quickly. Unlike investing, the return is guaranteed and equals your loan's interest rate. Unlike refinancing, there are no fees or paperwork. The math works for anyone with a loan, even if you can only afford a small extra amount. Run your numbers through a loan calculator — the savings are usually larger than people expect.